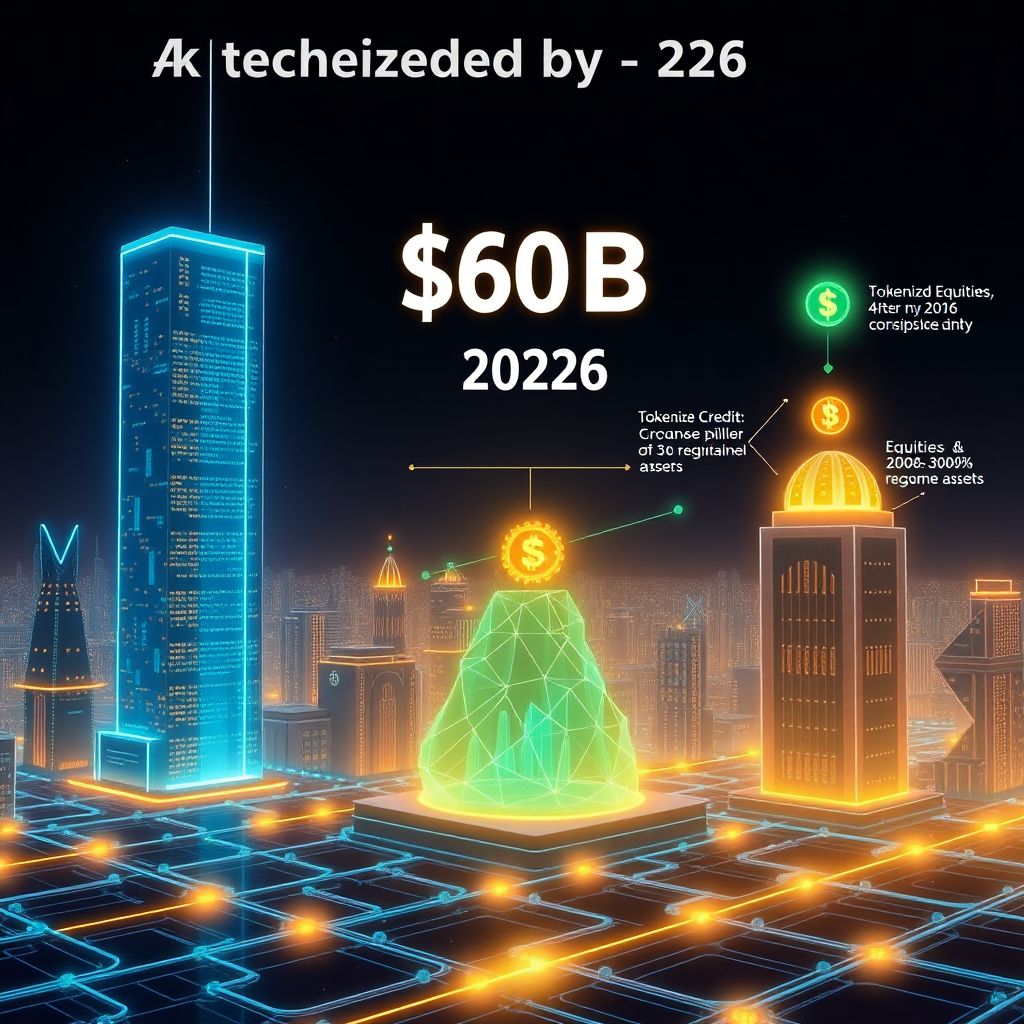

Tokenized real‑world assets are on track to become one of the most dynamic segments of digital finance, with their market value projected to hit around $60 billion by 2026. This forecast, based on analysis from blockchain oracle platform RedStone, underscores how quickly traditional financial instruments are moving on-chain and attracting institutional capital.

According to the report, the market began accelerating in late 2023, when large investors started paying closer attention to on-chain private credit, tokenized government bonds, and blockchain-based representations of stocks. What started as a niche experiment has evolved into a rapidly expanding ecosystem where conventional assets are mirrored, traded, and managed on distributed ledgers.

Private credit takes the lead

Within this emerging landscape, private credit stands out as the dominant category. RedStone’s estimates suggest that tokenized private credit will account for roughly 45–50% of the entire tokenized real‑world asset segment by 2026. This includes loans to businesses, trade finance products, and other forms of non-public lending that are being structured as on-chain instruments.

The appeal is clear: tokenization can streamline how these loans are originated, serviced, traded, and securitized. It also opens the door for a broader range of investors to gain exposure to yield-generating credit products that were historically difficult to access. For institutions, tokenized private credit offers improved transparency and programmability, while potentially reducing operational overhead and settlement friction.

Tokenized equities poised for explosive growth

While private credit may hold the largest share, tokenized equities are expected to be the fastest-growing category. RedStone projects that tokenized stocks could expand by 200–300% following a key regulatory inflection point anticipated in mid‑2026, particularly in the United States.

Market participants are watching for clearer rules on how tokenized shares should be issued, traded, and custodied. Once these regulatory questions are addressed, the expectation is that a wave of asset managers, brokers, and fintech platforms will move more aggressively into on-chain equity products. This could include tokenized versions of public company shares, synthetic equity exposures, and even tokenized fund units that track baskets of stocks.

The underlying promise is a more efficient, 24/7 equity market with fractional ownership, faster settlement times, and streamlined corporate actions such as dividend distribution and proxy voting executed directly via smart contracts.

Tokenized Treasuries gain institutional traction

Tokenized government securities, especially U.S. Treasuries, are another major pillar of the coming growth. The report highlights strong expected expansion in this segment, citing products such as BlackRock’s BUIDL fund as bellwethers for institutional adoption.

These on-chain Treasury products give investors exposure to one of the safest and most liquid asset classes in global finance while benefiting from the advantages of blockchain infrastructure. Institutions can manage cash, collateral, and liquidity more flexibly, moving tokenized Treasury positions between venues, protocols, or wallets in near real time.

This combination of safety, yield, and operational efficiency makes tokenized Treasuries a natural bridge for traditional finance players who want to gain blockchain exposure without venturing into more volatile crypto-native assets.

The role of RedStone and blockchain oracles

RedStone, the firm behind the report, operates as a blockchain oracle provider, delivering external data feeds to decentralized finance protocols. Oracles are a critical component of tokenized asset markets: they supply accurate, tamper-resistant price and reference data for instruments that exist off-chain in the traditional world.

For tokenized real‑world assets, this might include real‑time bond prices, interest rates, corporate actions, or credit event data. Without reliable oracles, smart contracts handling tokenized loans, bonds, or equities would not be able to function securely, making data providers like RedStone a foundational layer of the ecosystem.

Why tokenized real‑world assets are growing so fast

Several structural forces are driving the rapid expansion of tokenized assets:

– Search for yield and efficiency: Institutions are hunting for new ways to enhance returns while cutting settlement, custody, and compliance costs. Tokenization promises automated workflows, fewer intermediaries, and faster reconciliation.

– 24/7 global access: Unlike traditional markets bound by opening hours and local infrastructure, tokenized assets can trade continuously and be accessed worldwide, subject to regulatory restrictions.

– Fractional ownership: Large, illiquid assets can be split into smaller, tradable units, allowing a wider set of investors to participate.

– Programmable compliance and governance: Rules around who can hold or trade an asset can be embedded directly into the token’s logic, helping issuers manage complex regulatory obligations across jurisdictions.

As these benefits become more widely understood, more asset classes—from credit and sovereign bonds to real estate, commodities, and funds—are expected to migrate on-chain.

Institutional versus retail participation

The current wave of growth is largely institution-led. Private credit funds, asset managers, and corporate treasuries are experimenting with tokenized structures to improve capital efficiency and reach new investor segments. Tokenized Treasuries and credit instruments, in particular, align with the mandates and risk profiles of professional investors.

Retail adoption is still in the early stages, often constrained by regulatory requirements and know-your-customer procedures. However, as compliant platforms emerge and regulatory frameworks solidify, retail investors are likely to gain more controlled access to tokenized versions of traditional assets—potentially through regulated intermediaries and investment apps that abstract away blockchain complexity.

Regulatory clarity as a key catalyst

Regulation is both the main bottleneck and the strongest potential accelerant for tokenized markets. The anticipated mid‑2026 clarification of U.S. rules around tokenized securities is a central assumption behind RedStone’s forecast for 200–300% growth in tokenized equities.

Clear guidance on issues such as:

– how tokenized shares are classified,

– what licenses are required to issue and trade them,

– how custody and beneficial ownership are defined on-chain,

– how cross-border token distribution is treated,

will determine how quickly traditional institutions commit serious capital and resources. Jurisdictions that move faster to implement workable frameworks may become hubs for tokenized asset issuance and trading.

Opportunities and risks for market participants

For asset issuers and financial institutions, tokenization offers several opportunities:

– tapping new pools of capital,

– improving liquidity for previously illiquid instruments,

– reducing operational risk through automation,

– and differentiating products in a competitive market.

At the same time, there are significant risks and challenges:

– Technology and security: Smart contract vulnerabilities, key management failures, and cyberattacks can cause real-world losses.

– Legal enforceability: The relationship between on-chain tokens and off-chain legal claims needs to be watertight. Investors must have clear recourse if something goes wrong.

– Market structure risks: Fragmented liquidity across multiple blockchains and platforms can reduce efficiency and complicate price discovery.

– Regulatory uncertainty: Sudden changes in policy or enforcement posture could impact the viability of certain tokenization models.

Successful players will likely be those who combine strong technical execution with robust legal structuring and regulatory engagement.

How tokenization changes capital markets

If the market indeed grows to around $60 billion by 2026—and continues expanding beyond that—tokenization could begin to reshape how capital markets operate. Some possible long-term shifts include:

– Shorter settlement cycles as the norm: T+2 settlement may give way to near-instant finality structured around smart contracts.

– Integrated DeFi and TradFi workflows: Institutions could use decentralized protocols for collateral management, liquidity provision, or hedging, while still operating within regulated perimeters.

– More granular risk packaging: Instead of broad, opaque products, risk could be sliced into very specific tokenized tranches tailored to niche investor appetites.

– Greater transparency: Real-time visibility into asset flows, collateral positions, and ownership structures could improve risk monitoring for both regulators and market participants.

These changes will not happen overnight, but the projected growth in tokenized private credit, equities, and Treasuries suggests that the foundations are being laid now.

What to watch between now and 2026

Several developments will likely determine whether the $60 billion projection is met or exceeded:

1. Regulatory milestones in the U.S., Europe, and major financial centers regarding tokenized securities and on-chain market infrastructure.

2. Institutional pilot programs scaling into full production, especially in private credit securitization and tokenized bond issuance.

3. Interoperability solutions that connect different blockchains and legacy systems, enabling smoother asset transfers and unified liquidity.

4. Improvements in oracle infrastructure, ensuring reliable, low-latency data for complex real‑world assets.

5. Market stress tests, where tokenized markets are challenged by volatility, defaults, or operational incidents, revealing their resilience or fragility.

The interaction of these factors will shape whether tokenized real‑world assets remain a promising niche or become a central pillar of global finance.

In summary, RedStone’s outlook of a $60 billion tokenized asset market by 2026 rests on three main pillars: private credit as the dominant segment, tokenized equities as the fastest grower after regulatory clarity, and tokenized Treasuries as a trusted entry point for institutions. Coupled with maturing infrastructure and evolving rules, this convergence sets the stage for a profound transformation in how traditional assets are created, traded, and owned in the digital era.