SEC quietly drops crypto from 2026 exam priorities, signaling a major policy reset

The U.S. Securities and Exchange Commission has removed crypto from its list of explicit examination priorities for fiscal year 2026, in what amounts to one of the clearest breaks yet from the policy stance of the previous administration.

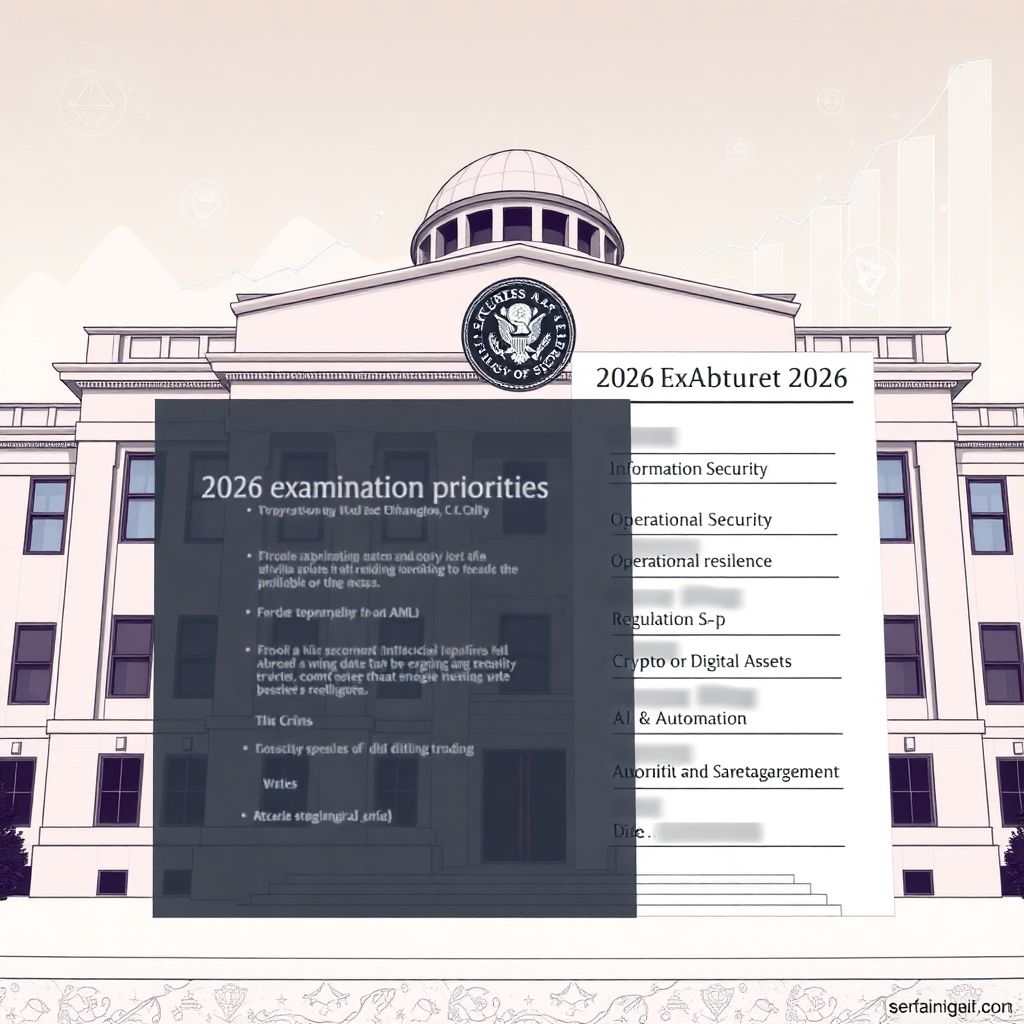

In the newly released “2026 Examination Priorities” for the Division of Examinations, the agency outlines where it plans to concentrate supervisory attention for investment advisers, funds, broker‑dealers, and key market infrastructures. Core themes dominate: information security, operational resilience, identity theft prevention, compliance with the updated Regulation S‑P, and anti‑money‑laundering controls.

But one topic that had been front and center for years is now absent: there is no standalone treatment of crypto or digital assets anywhere in the 17‑page document.

Crypto vanishes from the SEC’s stated risk map

The section devoted to “emerging financial technology” now focuses almost entirely on automated advisory tools, algorithmic trading systems, and the rapidly expanding use of artificial intelligence. Examiners are instructed to probe whether these tools generate recommendations that comply with existing securities laws and fiduciary standards.

Terms that had become standard in prior exam priorities — crypto assets, digital assets, virtual currencies, blockchain — are missing. They do not appear under fintech, AML, or any other category where digital assets had previously been framed as a discrete risk.

This stands in stark contrast to 2024 and 2025. Under the Biden administration, the 2024 exam blueprint included a dedicated section titled “Crypto Assets and Emerging Financial Technology,” explicitly stating that firms dealing in crypto assets and related products would face targeted scrutiny. The 2025 document again flagged crypto as a critical risk area, reinforcing a multi‑year pattern.

The 2026 omission, therefore, is not a mere editorial tweak. It is a clear signal that the SEC no longer intends to treat crypto as a separate risk category in its exam program, even as the asset class becomes more deeply embedded in mainstream financial products.

Realignment with new White House directives

The shift at the SEC does not exist in a vacuum. It follows a series of moves from the White House reshaping how federal agencies engage with digital assets.

Recent executive direction has pulled back on work related to a U.S. central bank digital currency, limiting further federal development on that front. At the same time, a President’s Working Group on digital asset markets has been set up to coordinate policy across agencies, suggesting a preference for a more centralized, high‑level strategic approach rather than fragmented, agency‑by‑agency initiatives.

The administration also unveiled plans for a Strategic Bitcoin Reserve and a federal stockpile of digital assets as part of a broader digital asset strategy. While the operational details of such reserves are still opaque, the messaging is clear: the federal government is no longer treating crypto solely as a threat vector, but also as a strategic asset.

New SEC chair, new regulatory tone

Leadership at the SEC has shifted as well. Paul S. Atkins, sworn in as SEC chair in April, has long been associated with a lighter regulatory touch and an emphasis on capital formation. His views align with one of President Trump’s long‑stated priorities: making the U.S. friendlier to crypto businesses and investors.

That political alignment is not purely rhetorical. Even before the inauguration, members of the Trump family had been launching or endorsing a broad array of crypto ventures — from a digital asset firm branded World Liberty Financial to memecoins tied to Trump and Melania. Collectively, public reporting estimates these efforts have generated more than $1 billion in profits for the family.

Against that backdrop, the SEC’s decision to stop highlighting crypto as a dedicated exam priority fits into a broader deregulatory, or at least de‑emphasized, approach to the sector.

Enforcement cools from earlier peaks

While the exam priorities relate to supervisory focus rather than enforcement directly, the broader enforcement trend is also telling.

Crypto‑related enforcement actions peaked recently. One research tally identified 46 crypto cases in 2023, the highest on record. In 2024, that number fell to 33, a decline of roughly 30% year over year.

Looking more broadly, the SEC closed fiscal 2024 with 583 total enforcement actions across all areas, a drop from the previous year. Yet the total financial remedies imposed hit an all‑time high of $8.2 billion, a figure significantly boosted by the blockbuster settlement with Terraform Labs.

Under the new chair, several longstanding, contentious crypto matters have been resolved or moved toward closure. The cumulative effect is a picture of an agency stepping back from constant escalation in digital asset enforcement, even if high‑profile cases still occasionally make headlines.

Crypto moves into the SEC’s core perimeter — without being named

Paradoxically, the removal of a dedicated crypto section comes just as digital assets are being woven more tightly into regulated products and institutions that sit squarely within the SEC’s jurisdiction.

The global crypto market capitalization rose sharply in mid‑2025, driven in part by institutional demand. U.S. spot Bitcoin exchange‑traded funds recorded strong net inflows throughout 2024, with continued interest through most of 2025. These products are now widely held by major asset managers, broker‑dealers, and retirement platforms — precisely the entities regularly examined by the SEC.

In other words, even without crypto being labeled as a separate risk category, the underlying exposure is being pulled into the regulatory perimeter via mainstream financial products. Examiners scrutinizing ETFs, advisory firms, and broker‑dealers will, in practice, be examining crypto exposure — just under the broader umbrellas of product suitability, disclosure, risk management, and operational resilience.

Market volatility persists despite policy softening

Market conditions, meanwhile, offer a reminder that regulatory de‑emphasis does not mean risk has disappeared.

After touching a peak in October, Bitcoin has since retreated. Ethereum has also weakened, with broader digital asset prices experiencing steep drawdowns in a compressed time frame. The rapid reversals underscore why prior exam priorities treated crypto as a distinct area of concern: extreme volatility, concentrated liquidity, and complex market structures can translate quickly into investor harm.

The absence of explicit crypto language in the 2026 priorities does not prevent the SEC from acting when fraud, manipulation, or misrepresentation emerge. But it does signal that the agency is less inclined to treat the entire asset class as inherently exceptional or uniquely hazardous.

Global regulators move in the opposite direction

While the SEC scales back crypto’s prominence in its exam agenda, international regulators are taking nearly the opposite path: building dedicated, sector‑specific frameworks for digital assets.

In the European Union, the Markets in Crypto‑Assets regime has now fully come into force. Rules for stablecoins have applied since mid‑2024, and the broader requirements for crypto‑asset service providers took effect at the end of that year. Stablecoins that failed to comply with the new standards faced delistings by early 2025, a concrete illustration of how assertively the framework is being enforced.

The United Kingdom has meanwhile advanced a draft legal instrument that would create new, explicitly regulated activities around crypto assets. Policymakers have launched consultations on trading venues, intermediaries, staking services, and elements of decentralized finance, signaling that a tailored crypto regulatory perimeter is coming.

Hong Kong has continued to refine its licensing regime for virtual asset trading platforms and rolled out a 12‑point “A‑S‑P‑I‑Re” roadmap in 2025. Among the more notable steps: enabling licensed platforms to share global order books with affiliated entities, a bid to improve liquidity while still maintaining regulatory oversight.

Singapore’s monetary authority has finalized and implemented a stablecoin framework for single‑currency stablecoins pegged to the Singapore dollar or G10 currencies. The framework, effective from 2024, sets out clear requirements around reserve assets, redemption, and governance, and is widely seen as a model for targeted, activity‑based digital asset regulation.

Collectively, these moves show many jurisdictions are not downgrading crypto as a priority; they are upgrading it into a formal, codified regime.

What the shift means for U.S. firms in practice

For market participants in the United States, the SEC’s change in exam priorities carries several practical implications:

1. Less “special treatment,” more integration into existing rules

Crypto is more likely to be assessed under familiar frameworks — suitability, disclosure, custody, AML, conflicts of interest — rather than through bespoke, crypto‑only initiatives. Firms should expect questions on how crypto fits into existing risk and compliance programs rather than whether they are “crypto firms” per se.

2. No guarantee of reduced enforcement risk

The absence of explicit mention in exam priorities is not a shield. If a product is deemed a security or if conduct violates existing rules, enforcement remains fully on the table. The SEC has repeatedly argued that most investor protections already apply to digital assets; the new stance seems to double down on that view.

3. More focus on AI, automation, and data security

Many crypto businesses rely heavily on automated trading, algorithmic strategies, and digital onboarding. With the SEC emphasizing AI and operational resilience, crypto platforms may still find themselves at the center of examinations — just from a different angle.

4. Compliance expectations will track institutionalization

As large asset managers, broker‑dealers, and retirement plans deepen their exposure to crypto‑linked products, the bar for governance and risk controls will rise. Firms cannot rely on regulatory ambiguity as a defense; examiners will expect standards similar to those applied to other complex products.

5. Regulatory arbitrage risk grows

With the EU, U.K., Hong Kong, and Singapore rolling out detailed regimes, U.S. firms face a patchwork of expectations when operating cross‑border. Being under‑regulated at home can quickly translate into being out of step abroad, especially on issues like stablecoin backing, consumer disclosures, and platform licensing.

Why the SEC might be stepping back from crypto‑specific labeling

Several strategic considerations likely underpin the SEC’s decision to remove explicit crypto language from the 2026 exam priorities:

– Political recalibration

A more pro‑crypto White House, coupled with a chair favoring capital formation, creates strong incentives to visibly soften the agency’s posture without explicitly rolling back existing enforcement wins.

– Regulatory fatigue and resource allocation

Years of high‑intensity crypto battles have consumed legal and human resources. As AI, cyber risk, and data privacy escalate, the SEC may be prioritizing these newer frontiers, viewing crypto as a more mature, integrated segment of the market rather than an emerging anomaly.

– Signaling normalization

Treating crypto simply as one asset class among many sends a message: digital assets are no longer an experimental fringe but part of the mainstream capital markets landscape. That normalization can encourage institutional participation while still allowing the SEC to act case by case.

– Litigation risk and legal uncertainty

The SEC has faced court setbacks that challenge the breadth of its jurisdiction over digital assets. By avoiding overt crypto labeling in exam priorities, the agency may be reducing the risk of future challenges that argue it is overstepping statutory authority.

Potential risks of de‑emphasizing crypto oversight

The policy shift is not without downside. Critics are likely to highlight several risks:

– Investor protection gaps

Retail investors remain heavily exposed to speculative tokens, high‑yield schemes, and opaque products. Without a targeted exam lens, subtle forms of misconduct or mis‑selling in crypto‑linked products may be harder to detect early.

– Systemic spillovers through ETFs and funds

As crypto exposure seeps into retirement accounts, mutual funds, and ETFs, failures or extreme volatility in digital asset markets can have broader consequences. A less explicit supervisory stance could underappreciate these linkages.

– Fragmented U.S. approach vs. cohesive foreign frameworks

While other jurisdictions crystallize dedicated crypto rules, the U.S. continues to rely heavily on enforcement, guidance, and interpretation. The absence of clear exam priorities risks reinforcing perceptions that the U.S. is neither fully welcoming nor fully predictable for digital asset businesses.

– Moral hazard and misread signals

Some firms may interpret the change as a green light to relax internal controls around crypto offerings. If that happens, the stage could be set for new waves of fraud or platform failures, prompting another abrupt regulatory swing.

How firms can adapt to the new landscape

Against this evolving backdrop, firms dealing with digital assets can take several steps to stay ahead of regulatory expectations:

– Embed crypto into enterprise‑wide risk frameworks

Rather than treating digital assets as a side project, integrate them into core risk, compliance, and governance processes. This aligns with the SEC’s shift toward treating crypto as part of mainstream operations.

– Reinforce AML and sanctions controls

Even if crypto is no longer singled out, AML remains a top‑tier priority. Firms should ensure that blockchain analytics, transaction monitoring, and onboarding processes are robust and well‑documented.

– Strengthen disclosures for retail products

Clear communication on volatility, liquidity risk, custody arrangements, and potential loss is essential. As institutional wrappers proliferate, the line between “traditional” and “crypto‑linked” products can blur; disclosures must not.

– Audit AI and algorithmic tools

With AI and automated advice under the microscope, firms using algorithms for trading, pricing, or customer recommendations should implement testing, documentation, and governance frameworks that can withstand exam scrutiny.

– Monitor evolving global standards

Multi‑jurisdictional firms, or those with international clients, should map their operations against rules emerging in the EU, U.K., Hong Kong, and Singapore, anticipating that elements of those regimes may inform future U.S. policy, even if indirectly.

A turning point, not an endpoint

The SEC’s decision to erase crypto from its 2026 exam priorities is best understood as a recalibration, not a retreat from the field. Digital assets are becoming more integrated into the traditional financial system, and regulators are adjusting from emergency response mode to a more normalized, risk‑based posture.

Whether this shift ultimately fosters innovation while preserving investor protection will depend less on what appears in a single priorities document, and more on how the SEC, the White House, Congress, and international counterparts continue to shape — or reshape — the rules of the game for digital assets in the years ahead.