Tether emerges as 2025’s top‑earning crypto protocol as stablecoins reshape the market

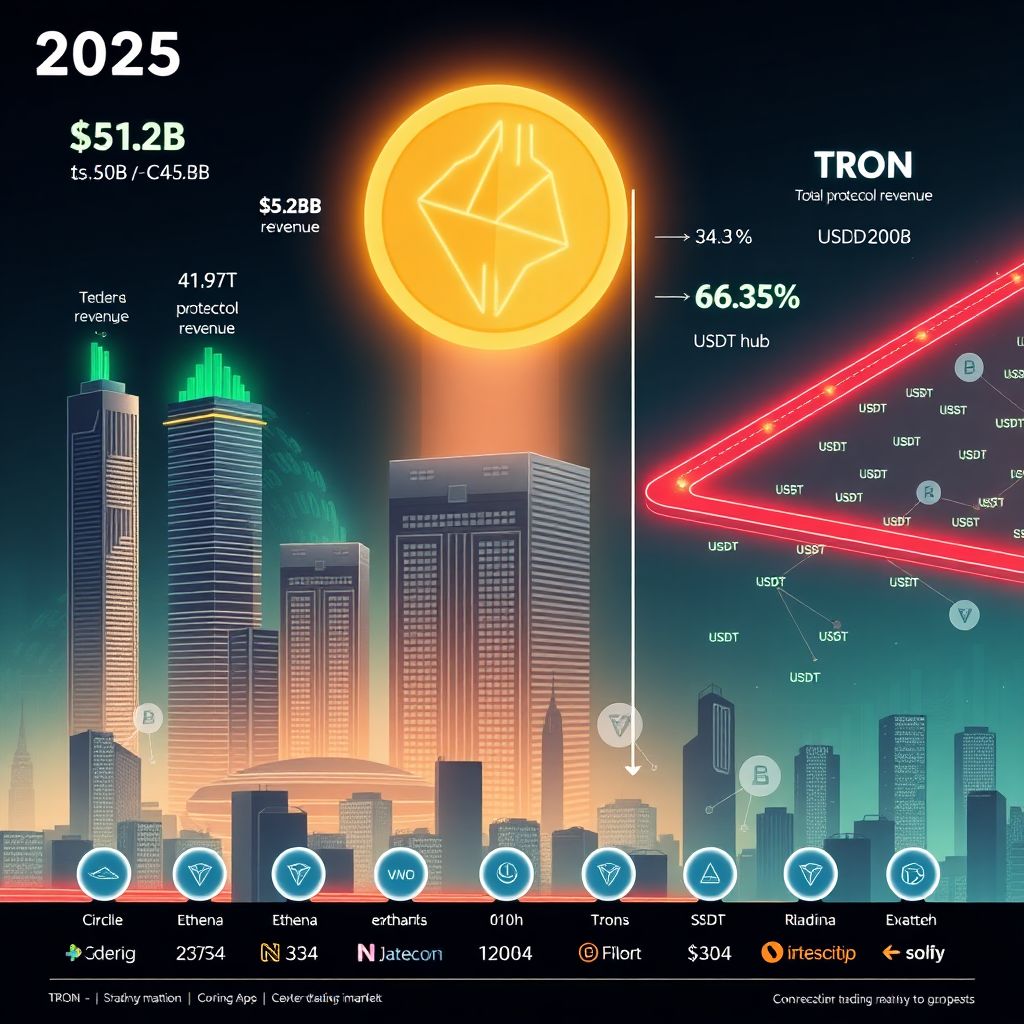

Tether closed 2025 as the most profitable crypto protocol worldwide, pulling in an estimated $5.2 billion in revenue. According to CoinGecko Research, that figure represented 41.9% of all income generated by 168 revenue‑producing crypto protocols over the year, underscoring how decisively stablecoins have moved to the center of the industry’s business model.

Stablecoin issuers as a group dominated the top of the rankings. Just four issuers – Tether alongside Circle, Ethena, and MoonTrade – were responsible for around 65.7% of total protocol revenue, or roughly $8.3 billion. In other words, two‑thirds of the sector’s protocol‑level income in 2025 came not from trading platforms, lending markets, or DeFi experiments, but from entities issuing tokenized dollars and similar assets.

Tron turns USDT demand into a revenue engine

Among base layer blockchains, Tron secured the second‑largest share of protocol revenue, with about $3.5 billion in 2025. This performance was largely tied to one factor: its position as the leading network for USDT transactions.

USDT’s heavy circulation on Tron created powerful network effects. High on‑chain activity translated into consistently strong fee revenue, even as other parts of the crypto market cycled between euphoria and drawdowns. Tron’s success shows how aligning a blockchain with a dominant stablecoin can turn transaction throughput into a predictable income stream.

Trading platforms fill out the top 10 – but on shaky ground

Rounding out the top 10 protocols were six trading‑focused platforms. While they enjoyed strong revenue during bullish phases – particularly early in the year – their business proved highly cyclical. Trading fees, liquidations, and speculative volumes all rose and fell with market sentiment.

This dependency became clear as 2025 unfolded. The year began with robust activity and rising income for exchanges and trading protocols, buoyed by speculative manias, especially around meme coins. However, the tone shifted dramatically after an historic liquidation cascade in October wiped out around $19 billion in leveraged positions. The resulting risk‑off mood cut deep into fee revenue, exposing how fragile trading‑driven business models can be in downtrends.

2025: the first annual crypto market decline since 2022

CoinGecko’s 2025 Annual Crypto Industry Report framed these revenue trends against a rare backdrop: a shrinking market. Total crypto market capitalization finished the year at about $3.0 trillion, down 10.4% compared with 2024. It was the first year‑over‑year decline since 2022.

Yet falling prices did not mean falling activity. Average daily trading volumes actually peaked in the fourth quarter at roughly $161.8 billion per day. Much of that volume stemmed from the October liquidation event and the heightened volatility that followed. The data highlights a crucial distinction: high trading volumes do not automatically translate into sustainable revenue if much of that volume is panic‑driven or short‑lived.

Trading protocol revenue whipsaws with market cycles

Trading protocols were the clearest victims of this boom‑bust dynamic. Their revenue trajectories in 2025 were defined by extreme swings tied to crowd psychology and speculative narratives.

A striking example came from Phantom, a leading trading platform during the Solana‑based memecoin craze. In January, at the height of that frenzy, Phantom generated around $35.2 million in revenue. As enthusiasm for meme coins cooled, so too did trading activity. By December, revenue had collapsed to roughly $8.5 million.

This rise‑and‑fall pattern repeated across many trading venues. Q1 was characterized by high engagement and fee income as traders chased fast‑moving opportunities. Once October’s liquidation shock rippled through the market, speculative interest dropped sharply. Bearish conditions in the final quarter caused trading protocol revenues to decline in tandem, despite overall market volumes remaining elevated for a time.

Throughout most of 2025, combined monthly protocol revenue across the industry hovered between about $3 billion and $3.5 billion. Within that relatively stable aggregate figure, however, the composition shifted: trading‑based income weakened, while stablecoin‑driven revenue held firm or expanded.

Stablecoins grow into a $311B pillar of the crypto economy

If speculators were pulling back, stablecoins were doing the opposite. Stablecoin market capitalization soared 48.9% over the course of 2025, adding roughly $102.1 billion in value to reach an all‑time high of about $311.0 billion.

This expansion was not simply a side effect of bull market exuberance – it persisted even as broader crypto asset prices declined. That resilience speaks to the role stablecoins now play as foundational infrastructure rather than just trading tools. They are used for remittances, payments, yield strategies, and treasury management, making them less sensitive to price cycles than many other crypto assets.

For issuers, this growth translated into some of the most reliable revenue streams in the sector. Income from reserves, fees, and associated financial products continued to flow even during periods when speculative trading dried up. Tether’s $5.2 billion in revenue is the clearest expression of this structural advantage.

PYUSD climbs into the top tier of stablecoins

A notable newcomer in 2025’s stablecoin landscape was PYUSD, issued under the PayPal brand. Over the year, PYUSD climbed to become the fifth‑largest stablecoin by market capitalization, growing 48.4% to reach approximately $3.6 billion.

Two drivers stood out. First, PYUSD gained traction as a payout option for YouTube creators, plugging it into the creator economy and giving it a clear, mainstream use case. Second, the token was integrated with a 4.25% yield offering via the Spark Savings Vault product, turning PYUSD from a simple transactional token into a yield‑bearing asset for users willing to park their capital.

PYUSD’s trajectory illustrates how strategic integrations and yield incentives can rapidly boost a stablecoin’s adoption, even in a competitive market dominated by incumbents like USDT and USDC.

Why stablecoins are outpacing the rest of crypto in revenue

The 2025 numbers crystallize a trend that has been building for years: stablecoins are evolving into the primary profit engines of the crypto ecosystem. Several structural factors explain their outperformance:

1. Consistent demand

Stablecoins function as digital cash and settlement currency. They are used in trading, lending, cross‑border transfers, and payments, creating continuous demand that is less directly tied to speculative bubbles.

2. Interest on reserves

Most fiat‑backed stablecoins are backed by high‑quality, interest‑bearing assets such as short‑term government securities. In a higher interest rate environment, these reserves generate significant income for issuers, which can far exceed their operating costs.

3. Lower volatility risk

Because stablecoins aim to maintain a peg, users are less exposed to wild price swings. This makes them more attractive for businesses, institutions, and payment use cases than volatile native tokens, encouraging broader adoption.

4. Composability in DeFi

Stablecoins are the base asset for many decentralized finance applications. This central role allows issuers to partner with protocols, launch yield products, and tap into additional revenue streams beyond simple issuance.

Tether’s dominance in 2025 is a direct consequence of sitting at the intersection of these forces, with USDT deployed across multiple chains and use cases at massive scale.

Tron’s lesson: traffic follows stablecoins, and fees follow traffic

Tron’s $3.5 billion in blockchain revenue underlines another important theme: blockchains that succeed in becoming stablecoin hubs can generate robust income even if they are less prominent in other areas, such as DeFi experimentation or NFT ecosystems.

USDT users gravitate toward Tron because of low fees, fast confirmations, and established liquidity. In return, Tron benefits from high throughput, which fuels transaction fees and related revenues. This symbiotic relationship suggests that for many networks, winning the stablecoin flow war could be more important than competing on headline‑grabbing narratives.

Other chains are taking note, optimizing their infrastructure to better support stablecoin transfers, institutional PoS rails, and compliant payment layers. The 2025 data reinforces that the “payments and settlement” niche, rather than pure speculation, may drive sustainable protocol earnings over the long term.

DATCos quietly accumulate BTC and ETH – then hit a wall

While stablecoins and their host networks grabbed the revenue spotlight, another structural shift unfolded in the background: the rise of Digital Asset Treasury Companies (DATCos). These entities collectively deployed at least $49.7 billion in 2025 to acquire more than 5% of the combined supply of BTC and ETH.

This large‑scale accumulation reflects a growing belief in digital assets as strategic reserves, akin to corporate or sovereign holdings of gold. However, the pace of deployment slowed sharply in the fourth quarter, dropping to about $5.8 billion.

The slowdown was not due to a loss of interest in BTC and ETH themselves but to market pressure on DATCo shares. As crypto prices fell and volatility spiked, many of these companies saw their own valuations decline. That forced several to prioritize share buybacks and balance‑sheet defense over continued aggressive accumulation, highlighting how equity market dynamics can constrain long‑term accumulation strategies.

Revenue resilience vs. price performance: a new way to judge protocols

One of the key takeaways from 2025 is that price appreciation and protocol revenue are not always aligned. The total crypto market cap declined, yet some protocols – especially stablecoin issuers and select blockchains like Tron – posted record or near‑record revenues.

For investors, builders, and analysts, this suggests a shift in how protocol success should be evaluated. Rather than focusing solely on token price or TVL (total value locked), there is growing importance in metrics such as:

– Share of total protocol revenue

– Stability of revenue through market cycles

– Dependence on speculative activity vs. structural demand

– Distribution of revenue among tokens, validators, or shareholders

Stablecoins score strongly on most of these metrics, which explains why they have quietly become the most economically powerful category in crypto, even if their prices are designed not to move.

What 2025 signals for the next phase of crypto

The 2025 landscape paints a clear picture of where the industry is heading:

– Stablecoins are no longer a side product – they are the core financial infrastructure of the crypto economy and its most reliable source of revenue.

– Blockchains aligned with stablecoin flows – like Tron with USDT – can thrive on transaction income without leading every innovation wave.

– Trading‑centric protocols remain highly cyclical – lucrative in bull runs but exposed when markets turn risk‑off.

– Institutional and corporate players – through DATCos and similar vehicles – are steadily transforming BTC and ETH into strategic reserves, even if their accumulation pace varies with equity market sentiment.

As the industry moves beyond purely speculative cycles, protocols and businesses that resemble traditional financial infrastructure – payment rails, settlement networks, and reserve‑backed instruments – appear best positioned to generate durable, recurring revenue. Tether’s 2025 performance is likely not an outlier, but an early indicator of a more mature, cash‑flow‑driven phase of the crypto market.